Italy is the fourth-largest national economy in Europe and is in the top 10 for the gross domestic product (GDP) in the world. Economically, Italy relies mostly on services and manufacturing, with the services sector accounting for almost three quarters of GDP and industry accounting for a quarter of the country’s production. Manufacturing is the primary sub-sector within industry. In terms of size, Italy’s population is around 59.7 million.

Italy is the fourth-largest national economy in Europe and is in the top 10 for the gross domestic product (GDP) in the world. Economically, Italy relies mostly on services and manufacturing, with the services sector accounting for almost three quarters of GDP and industry accounting for a quarter of the country’s production. Manufacturing is the primary sub-sector within industry. In terms of size, Italy’s population is around 59.7 million.

The Italian pharmaceutical industry is one of the largest in the world, even though its position in the ranking is decreasing due to the entry of emerging markets such as China and Brazil (5th in 2005, 6th in 2013, and expected to be 7th in 2017), says Anna Baudo, managing director of Keypharma, part of ProductLife Group.

Italy ranks No. 1 in the world for exports — about 70% of Italian production is exported — and No. 2 in Europe for production volume, both in absolute and per capita terms.

The Pharma Market

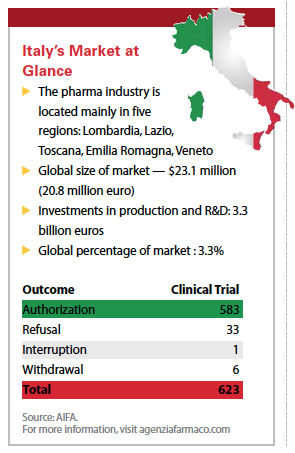

According to National Institute of Statistics data, Italy has 174 manufacturing production units; 62,000 employees; 6,000 engineers in R&D; €27 billion euros ($30.39 billion) in sales and €2.4 billion in investments, half of which are allocated in R&D.

Lorenzo Positano, a consultant, says the pharma market in Italy is valued at $22 billion, but compared with other European markets it’s declining slightly, ranging between 3% and 4% growth on a compounded average rate until 2020.

“This is mostly due to a decline in sales of patented drugs while generics and OTCs are increasing; OTCs have sales of between 2% to 3% per year and generics at 1%," Mr. Positano says. “In particular, generics have had enormous growth in the past few years due to fact that generics were severely underrepresented on the Italian market, and in fact still are — generics account for 25% of the market in terms of sales and 40% in terms of volume. This is low compared with other European and global markets."

“This is mostly due to a decline in sales of patented drugs while generics and OTCs are increasing; OTCs have sales of between 2% to 3% per year and generics at 1%," Mr. Positano says. “In particular, generics have had enormous growth in the past few years due to fact that generics were severely underrepresented on the Italian market, and in fact still are — generics account for 25% of the market in terms of sales and 40% in terms of volume. This is low compared with other European and global markets."

Carlo Silenzi, managing director, Kantar Health Italy, notes that the pharmaceutical market grew by 3% in 2014, driven by positive growth in the hospital channel (+5%) and distribution on behalf of local health authorities (+25%), and a negative trend in the retail channel.

“The decrease in turnover for the retail distribution of prescription products is due mostly to the decrease in the average price and the increase of the generic drugs prescriptions," Mr. Silenzi says.

Despite a fall in Italy’s GDP between 2008 and 2013, pharmaceutical production rose by 2% and the productivity rate by 4% per year, the highest rate of any economic sector, Ms. Baudo notes. But at the same time the workforce has dropped by 17% over the past decade, while still remaining the leading employer in the Italian manufacturing sector.

Among all of the big pharma companies in Italy, however, Mr. Positano says there are no big Italian pharma companies akin to France’s Sanofi or Germany’s Merck KGaA, Bayer, and Boehringer Ingelheim.

“The biggest pharmaceutical company is Menarini, which in terms of revenue is $4 billion, but if you look at the ranking of the pharma companies, it’s only about 38 or 40 in world," he says.

Mr. Positano attributes Italy not having any truly big pharma companies to the fact that there has been no government intervention to develop the pharma market.

Mr. Positano attributes Italy not having any truly big pharma companies to the fact that there has been no government intervention to develop the pharma market.

The R&D Sector

In terms of investment in R&D, pharma is the second-largest manufacturing sector in Italy, behind aeronautics and transportation, accounting for 12% of total manufacturing investments, Mr. Silenzi says.

He notes that in 2013 total investment in R&D was €1,220 million euros, with 5,950 R&D employees, or 9.6% of pharma employees, a significantly higher share compared with all industries at 0.6%.

“This clearly shows the importance of the sector within the Italian economy," he says.

However, Mr. Positano says while there is investment in R&D it’s not consolidated and companies aren’t investing in large R&D facilities in Italy.

“There are a few pockets of excellence but we don’t have the investment levels of expertise to compete with other innovation labs across the world or in other countries in Europe," he says. “The government is trying to take steps to support the life-sciences sector but at the moment there is no specific government initiative."

“There are a few pockets of excellence but we don’t have the investment levels of expertise to compete with other innovation labs across the world or in other countries in Europe," he says. “The government is trying to take steps to support the life-sciences sector but at the moment there is no specific government initiative."

Ms. Baudo says more than 90% of pharmaceutical research in Italy is funded by pharmaceutical companies.

“The Italian R&D pipeline is financed by the industry, mainly by small- to medium-sized enterprises in the early stages of development — 112 projects out of 154 — and then in Phase II and III studies by big pharma companies — 204 projects out of 249," she says.

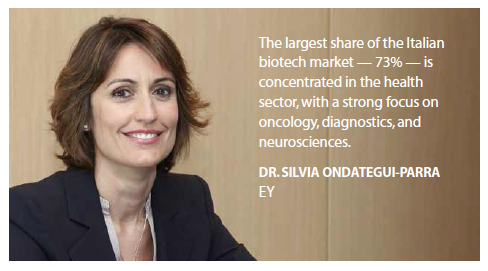

The pharma sector in Italy has a very high percentage — 81% — of companies performing innovative activities, a statistic that places the country second in Europe again, behind Germany, says Silvia Ondategui-Parra, M.D., Ph.D., partner, MED healthcare & life sciences leader and global market access & reimbursement leader at EY.

According to Gilbert D’Ambrosio, head of commercial business development for Southern Europe, Quintiles, the biotech sector is highly productive and expanding rapidly. Overall, the biopharmaceutical pipeline includes 403 products — 44 more products compared with last year — 108 of which are in the preclinical phase; 46 in Phase 1; 126 in Phase II, and 123 in Phase III of clinical trial development.

In addition there are also 67 projects in the discovery phase, Mr. D’Ambrosio says. He adds that almost half of the projects are biotech products (45%), such as monoclonal antibodies (26%), recombinant proteins (10%), products for cell therapy (3%), gene therapy (4%) and regenerative medicine (2%).

“The main therapeutic area for biotech research is oncology, with 40% of projects in clinical development, followed by autoimmune and inflammatory diseases, 13% of projects; neurology, 9% and metabolic, hepatic and endocrine disorders, 9% of projects," he says.

“The main therapeutic area for biotech research is oncology, with 40% of projects in clinical development, followed by autoimmune and inflammatory diseases, 13% of projects; neurology, 9% and metabolic, hepatic and endocrine disorders, 9% of projects," he says.

In 2013, Europe granted marketing authorization to the first product resulting from the research by an Italian biotech company. This product, defibrotide, is a life-saving drug developed by Gentium, used in the treatment of severe hepatic veno-occlusive disease (VOD) in patients undergoing hematopoietic stem cell transplantation (HSCT) therapy, Mr. D’Ambrosio says.

Dr. Ondategui-Parra says while the country has a strong domestic pharmaceutical industry, there are some factors that have reportedly negatively impacted the investment in pharmaceutical R&D.

“Among the many factors that might render the Italian market less attractive to the major multinational players when launching new pharmaceuticals are the more difficult launch requirements compared with other EU players, including the strict pricing regime," she says. “Moreover, many multinationals believe the climate is still unstable, as a consequence of the economic crisis, and remain uncertain about investing in the country."

Access to Medicines

According to Dr. Ondategui-Parra, expenditure on new drugs is lower in Italy than in other major European markets. Public pharmaceutical spending is more than 25% lower than the average across large EU countries at 270€ compared with 370€ in per capita terms.

“Only 35% of the medicines approved by the EMA between 2011 and 2013 were available for reimbursement in Italy, compared with 69% in Germany, 66% in the U.K., and an average of 52% throughout Europe," Dr. Ondategui-Parra says.

There are also significant market access delays in Italy, she says. The overall time to market for new medicines is more than two years.

As a country, Italy has one of the highest number of regulatory hurdles to overcome, which slows access to the market, and as a result Italy registered the lowest number of new drugs launched in EU countries between 2001 and 2013.

As a country, Italy has one of the highest number of regulatory hurdles to overcome, which slows access to the market, and as a result Italy registered the lowest number of new drugs launched in EU countries between 2001 and 2013.

“The process from EMA approval until the medicine is actually available on the Italian market takes on average 427 days, compared with 80 days in Germany, 109 in the U.K., and an average of 221 days throughout Europe," Dr. Ondategui-Parra says. “Even after market access, new products are penalized by several restrictions."

On the other hand, medicines in Italy are priced approximately 15% lower than in the U.K., Germany, Spain, and France, Dr. Ondategui-Parra says.

Ms. Baudo points to a number of steps being taken to improve time to market through legislation that creates a new class of drugs, named Cnn (class non-negotiated), which could be included within 60 days of approval, allowing companies to launch after notification to AIFA of the price they intend to apply. Subsequently, companies can apply for Pricing & Reimbursement (P&R).

In the case of highly innovative products, orphan drugs, and products targeted to exclusive hospital use, the P&R application can be submitted before the marketing application, following approval by the Committee for Medicinal Products for Human Use (CHMP) or AIFA approval (depending on the procedure).

Moreover, the so-called 100-days procedure allows fast-track approval for the P&R orphan drugs and products showing exceptional therapeutic importance.

“To date, timelines imposed by law are not 100% respected, but the trend is positive and AIFA cancelled the massive backlog that negatively affected the time to market of the majority of product launches in Italy until few years ago," Ms. Baudo says.

Clinical Trials

Italy has a strong clinical studies background with proven capabilities to enroll patients and it has globally recognized centers of excellence particularly to manage Phase II studies, says Antonio Irione, EY Italy life sciences leader.

Italy has a strong clinical studies background with proven capabilities to enroll patients and it has globally recognized centers of excellence particularly to manage Phase II studies, says Antonio Irione, EY Italy life sciences leader.

A total of 3,387 clinical trials were started in Italy between 2009 and 2013, 65.9% of which were sponsored by the pharmaceutical industry — for-profit studies — and 34.1% of which were publicly sponsored studies, Mr. D’Ambrosio.

But meeting timelines can be a challenge, which Mr. Irione says is mainly due to delays by the ethics committees. Italian legislation requires that any clinical trial must be submitted and approved by an ethics committee before getting the green light to go ahead.

“To improve efficiency many regions are currently reviewing these procedures and trying to establish a faster process with particular regard to those trials already approved at regional level and for those hospitals meeting specific excellence criteria from a trial perspective," he says. “This new operating model would limit delays while maintaining a quality approach."

Mr. Positano says while Italy has a large number of clinical facilities in terms of hospital beds — No. 2 or No. 3 in Europe — in terms of clinical studies per beds, Italy is only fifth or sixth in Europe, so it is not making optimum use of its clinical facilities.

He adds there has been a slight decline in clinical trials initiated in Italy, declining 3% to 4% per year.

“This is probably because Italy is costly for doing clinical studies — we rank fourth or fifth in terms of cost per patient in the world; for example, it’s less expensive to do trials in the United States than in Italy," Mr. Positano notes.

However Mr. D’Ambrosio notes that the decline in clinical studies is in line with the general trend in Europe, adding that Italy has an EU market share of 17.2% in interventional drug research.

One trend that has emerged is a move to specific agreements between pharma companies and regions, Mr. Irione says.

“Such agreements enable both a specific number of clinical studies to take place in the region as well as for the process from national to hospital approval to be accelerated in that region," Mr. Irione says.

The Healthcare and Reimbursement Environment

The Italian healthcare system, much like the Spanish one and as opposed to all other countries in Europe, is decentralized. It operates on three levels: national, regional and local, Dr. Ondategui-Parra says.

Healthcare expenditure as a percentage of GDP is roughly 20% lower than in other large European countries, and for pharma spending the gap is about 30%, she adds.

According to Ms. Baudo, the low spending on health is despite the fact that Italy’s population is older than the EU average.

“This is the result of the multiple cost-containment measures put in place since the early 1990s, which ranged from delisting some drugs to price cuts, discounts, reimbursement limits, risk-sharing agreements, per-product and company annual sales caps, and consequent clawback mechanisms, just to list some of the measures adopted," Ms. Baudo says.

In terms of product approval, products are either approved at the EU level or at a national level, in which case companies apply through the Italian drug agency, AIFA, Mr. D’Ambrosio says. Italy can also act as the reference member state or the concerned member state for applications through the decentralized and mutual recognition procedures.

Italy’s healthcare system is highly regional. Mr. Silenzi notes that while healthcare policy (Piano Sanitario Nazionale; PSN) and reimbursement are determined nationally, the regional governments implement the PSN with their own resources and can make adjustments to suit the specific needs of the region, including setting patient co-payments.

Pharmaceutical companies negotiate with AIFA on the prescription criteria and then reimbursement, Mr. Irione says. More and more reimbursement is based on pay-per-performance criteria, for example with the company having to make payments if the drug fails to meet therapeutic goals, or a capped level, whereby sales exceeding an assigned cap must be paid back to AIFA.

The methods used in Italy to determine the pricing and reimbursement level of new drugs have changed markedly over the years, Mr. D’Ambrosio says.

“Before 2004 the pricing and reimbursement system was based on two systems: the European Average Price (EAP), determined according to criteria defined by the Inter-Ministerial Committee for Economic Planning (CIPE), part of the Ministry of Economy, and the calculation derived from the weighted average of the prices of most packages sold in EU with the same active molecule and way of administration," he says.

After the Jan. 1, 2004, the prices of all the medicines reimbursed by the National Health Service (NHS) have been defined by negotiation procedures established by CIPE in 2001. In addition, pharmacoeconomic criteria, such as positive cost/efficacy ratio, a favorable benefit/risk profile, economic impact on the NHS, and market share of the medicinal product have been taken into consideration, Mr. D’Ambrosio notes.

Once a product is approved by AIFA, the drug needs to be included in regional therapeutic formularies before it is allowed to be sold.

“Different regions have different registration criteria procedures," Mr. Irione says. “Regions could apply additional restrictions to drug both in terms of authorized prescribers and access to patients."

Mr. Positano says Italy has 21 regions that are responsible for healthcare expenses so companies have 21 stakeholders to manage.

After that, a new drug must also be listed within the hospital formulary before it can be sold. Some regions are now defining some fast-track registration criteria to accelerate drug availability to the patients, Mr. Irione says.

“Southern Italy has comparatively little economic development compared with the north," Mr. Silenzi says.

“Northern Italy is part of the ‘blue banana’, the main corridor of economic activity in Europe."

Mr. Silenzi says that significant differences between north and south are seen in health-related impairment both at work and at home.

“Those currently residing in the Mezzogiorno, the south, had 28% higher health-related work impairment than those residing in the north," he says. “Across the entire population residents of southern Italy were 19% more impaired in non-work activities."

Ms. Baudo also notes that the fragmented reimbursement procedures result in a multitude of regional and local access gates, and a creative list of access processes that slow down a drug’s commercialization, which has an impact on budgets. (PV)